The Basics of Financial Resilience for Young Adults

Understanding Financial Resilience: What It Means

Financial resilience is the ability to withstand economic challenges while maintaining stability. For young adults, this means being prepared for unexpected expenses like car repairs or medical bills. It's about having a safety net that allows you to navigate life's ups and downs without falling into debt.

It's not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.

Think of financial resilience like a strong tree in a storm. Just as a tree's deep roots help it weather harsh winds, your financial habits can help you stay grounded during tough times. The stronger your financial foundation, the less likely you are to be uprooted by unforeseen challenges.

Ultimately, building financial resilience is about creating a buffer that protects you from financial stress. By understanding what it entails, you can start laying the groundwork for a secure financial future.

Creating a Budget: Your First Step to Resilience

A budget is your roadmap to financial resilience. It helps you track your income and expenses, ensuring you know exactly where your money is going each month. By setting clear spending limits, you can prioritize essential expenses while finding room for savings.

Imagine budgeting like packing a suitcase for a trip. You want to make sure you have enough space for all your essentials while avoiding unnecessary items that could weigh you down. Similarly, a well-planned budget helps you allocate your resources wisely, giving you more freedom in the long run.

Build Financial Resilience Early

Establishing a budget and emergency fund creates a strong foundation for navigating unexpected financial challenges.

Start by listing your income sources and monthly expenses, then categorize them into needs and wants. Adjust your spending habits based on your priorities, and you'll quickly see how budgeting can enhance your financial resilience.

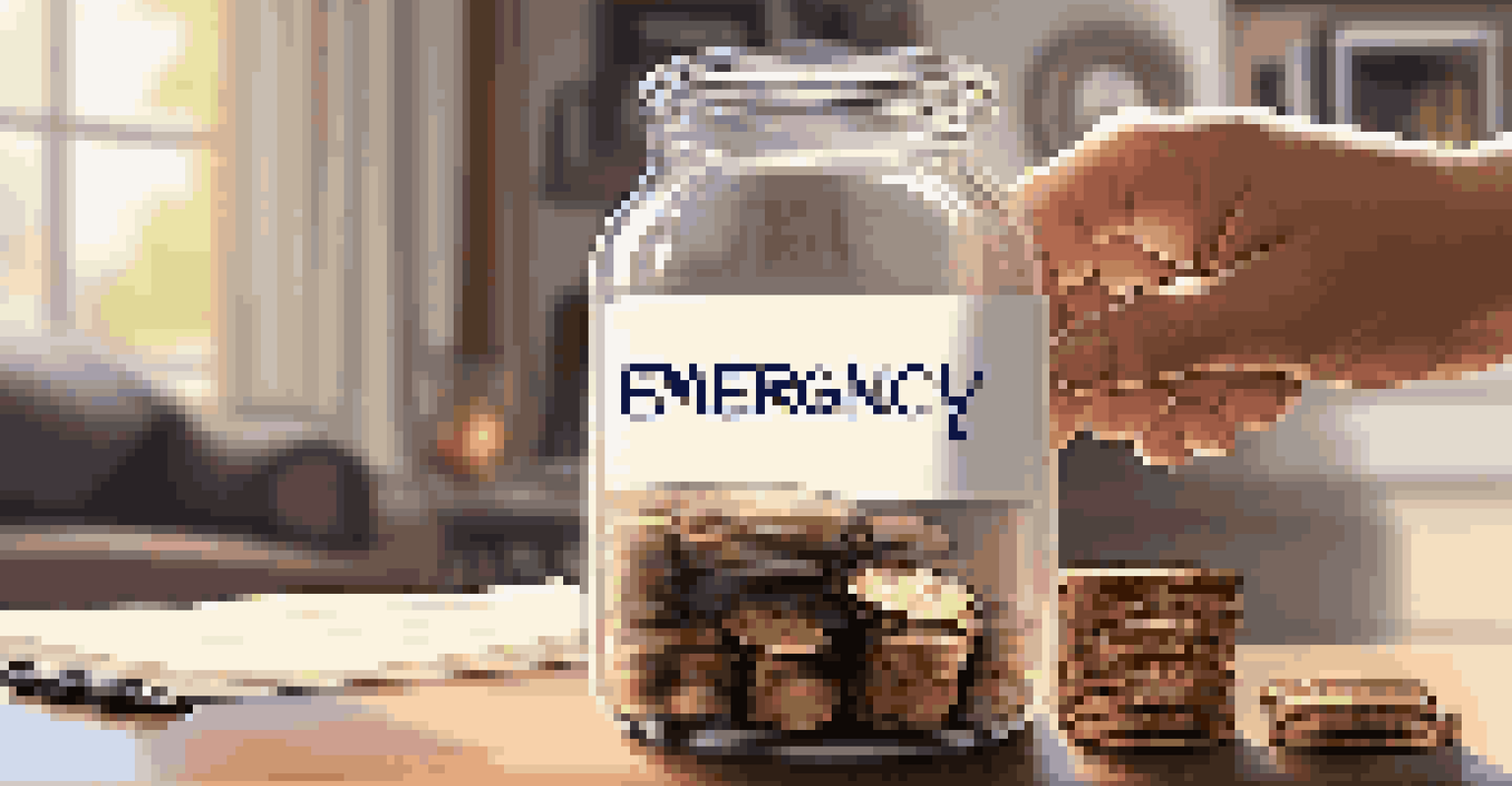

Emergency Funds: Your Financial Safety Net

An emergency fund is a crucial part of financial resilience, acting as your safety net in times of crisis. This fund should ideally cover three to six months' worth of living expenses, ensuring you can handle unexpected situations without going into debt. Think of it as a financial cushion that softens the impact of life’s surprises.

The best time to plant a tree was twenty years ago. The second best time is now.

Creating this fund might feel daunting, but starting small can make it manageable. Even setting aside a little money each month can add up over time, providing you with peace of mind. Just like saving for a dream vacation, each contribution gets you closer to your goal, but here, the goal is security.

When you have an emergency fund, you're less likely to panic during financial setbacks. You'll feel empowered to make informed decisions rather than reacting impulsively, which is a key component of long-term financial resilience.

Smart Saving Strategies for Young Adults

Saving money doesn't have to be overwhelming; it can actually be quite rewarding. Start by identifying specific goals, whether it's a vacation, a new gadget, or a down payment on a car. By focusing on clear objectives, saving becomes more motivating and purposeful.

A popular strategy is the 50/30/20 rule: allocate 50% of your income to needs, 30% to wants, and 20% to savings. This simple framework helps you balance enjoying your money now while still preparing for the future. Think of it as a way to enjoy the journey while still keeping your destination in sight.

Understand Debt Types

Differentiating between good and bad debt is crucial for maintaining financial stability and resilience.

Don't forget to automate your savings! Setting up automatic transfers to your savings account can help you build your fund effortlessly. Just like brushing your teeth becomes a routine, saving can become a natural part of your financial life.

Understanding Debt: When It Becomes a Problem

Debt can be a slippery slope, especially for young adults. While some debt, like student loans, can be a part of investing in your future, it's crucial to differentiate between 'good' and 'bad' debt. Good debt typically helps you build wealth, while bad debt can lead to financial strain if not managed properly.

Consider debt like a double-edged sword. It can provide opportunities, such as funding education or a home, but it can also cut into your financial stability if it spirals out of control. Being aware of the type and amount of debt you carry is essential for maintaining resilience.

Regularly reviewing your debt situation can help you stay on top of payments and avoid falling behind. If you find yourself overwhelmed, seeking advice or restructuring your debt can be a smart move toward regaining control.

Investing Basics: Growing Your Wealth Early

Investing may seem intimidating, but starting early can significantly enhance your financial resilience. The earlier you begin investing, the more time your money has to grow through compound interest, which is essentially earning interest on your interest. It's like planting a tree; the sooner you plant it, the larger it can grow over time.

Consider starting with low-cost index funds or a retirement savings plan, which can provide a diversified investment without requiring a lot of knowledge. Even small contributions can make a difference, so don’t underestimate the power of getting started now.

Investing for Future Security

Starting to invest early allows your money to grow and enhances your long-term financial resilience through compound interest.

Remember, investing isn't just for the wealthy; it's a crucial part of building long-term financial security. By educating yourself and taking advantage of available tools, you can set yourself up for a more resilient financial future.

The Importance of Financial Education for Young Adults

Financial education is the cornerstone of financial resilience. Understanding how money works, including budgeting, saving, and investing, empowers you to make informed decisions. Just like learning a new skill, the more you know, the more confident you become in your financial abilities.

Think of financial education as a toolbox. Each tool represents a different skill or piece of knowledge that helps you tackle various financial challenges. The better equipped you are, the easier it is to navigate your financial landscape and build resilience.

Utilize resources like online courses, workshops, and books to enhance your financial literacy. Start small and gradually expand your knowledge base, and you'll find that understanding your finances becomes second nature.